French

French

In its latest session, Lebanon’s Council of Ministers approved the appointment of Karim Souaïd as the new governor of the Central Bank, with 17 votes in favor and seven against. What stood out, however, were the reservations voiced by Prime Minister Nawaf Salam in his post-session remarks, hinting at potential cooperation issues down the line between the premiership and the Central Bank’s new leadership.

The appointment is undeniably a crucial development given the central role the Central Bank plays, especially in the current economic and monetary crisis. Leaving this position vacant was no longer viable, and filling it should be seen as a positive step for the government and the presidency—regardless of the appointee’s identity.

Based on his publicly circulated résumé, Karim Souaïd appears qualified for the role. He has extensive experience in finance, banking, and law, having worked in investment banking, asset management, and regulatory compliance. He has collaborated with finance ministries and central banks across several Arab countries, and his expertise includes financial restructuring, capital markets, and privatization initiatives. His professional journey includes roles at HSBC and his own firm, Growthgate Equity Partners. Souaïd also holds a degree in banking law from Harvard University.

Criticism of Souaïd has centered not on his qualifications but on his ties to the banking sector, his endorsement of a controversial Harvard study that proposes converting bank deposits into government bonds, and his apparent lack of enthusiasm for negotiating with the International Monetary Fund (IMF). Prime Minister Salam also emphasized the importance of the Central Bank aligning with the government’s fiscal policies.

According to Article 19 of Lebanon’s Code of Money and Credit, the Central Bank governor cannot be dismissed except in cases of voluntary resignation, health-related incapacity, serious misconduct as defined by the Penal Code, or gross mismanagement. The same criteria apply to the deputy governors.

Article 26 grants the governor broad powers to manage the bank’s operations and implement the Code’s provisions. This legal framework ensures the Central Bank’s independence in executing its mandate. As outlined in Article 70, this includes maintaining the stability of the Lebanese pound, ensuring economic stability, safeguarding the banking sector, and developing the financial markets. The government’s involvement is limited to the participation of the director generals of the Finance and Economy Ministries—both ex-officio members of the Central Council (Article 28)—and oversight through the government commissioner (Articles 41 and 42).

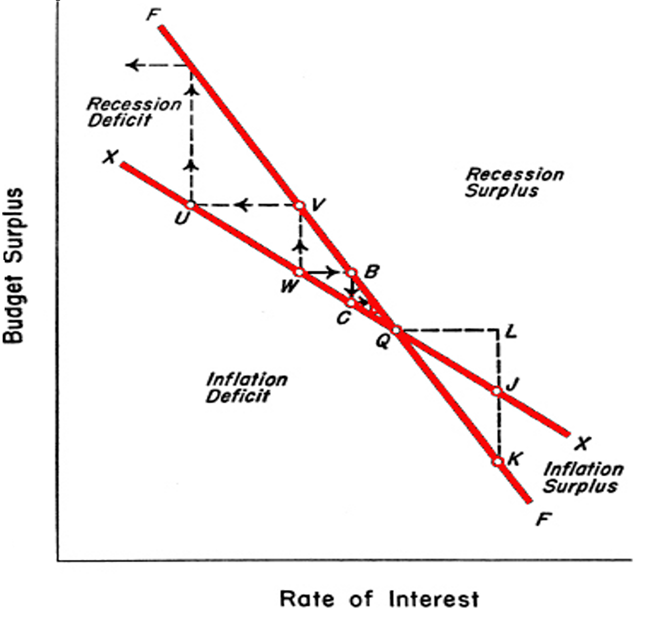

Economically, this independence is designed to prevent the government from using monetary policy as a backdoor for hidden taxation via excessive money printing—an undemocratic practice that would bypass parliamentary approval. Still, independence does not preclude cooperation. Exchange rate policy, for instance, is set by parliament (Article 229), and major reforms, like restructuring the banking sector, require legislative action. Economically speaking, currency exchange rates reflect both internal (price stability and full employment) and external (balanced current account) equilibriums—a result of collaboration between fiscal and monetary policies (see Chart 1).

Chart 1: Exchange Rate value as a Function of Fiscal and Monetary Policy Coordination (Source: Wong et al., 2002)

Chart 1: Exchange Rate value as a Function of Fiscal and Monetary Policy Coordination (Source: Wong et al., 2002)

Back to the concerns surrounding Souaïd’s appointment—many of the major reforms fall under the government and parliament’s jurisdiction, not the Central Bank’s. The governor’s role is to implement laws, with the Central Council focused primarily on Article 70’s mandate. Therefore, any concerns about his powers must be viewed through the proper legal lens, particularly as the Central Bank remains under the broader authority of the government and legislature.

Souaïd faces a long list of daunting challenges: tackling Lebanon’s cash-based economy, dealing with the controversial "Qard al-Hassan" financial institution, shaping monetary policy, outlining a banking sector restructuring plan, resolving the deposit crisis, and securing liquidity to stabilize the Lebanese pound and protect depositors.

The “Qard al-Hassan” file is highly political. Souaïd essentially has two options: pursue legal action against the institution for operating without a Central Bank license or attempt to bring it under regulatory control by licensing it as a financial institution. The latter would involve complex regulatory and financial negotiations led by Lebanon’s Banking Control Commission.

On the cash economy, the governor must propose a strategy to combat the phenomenon that landed Lebanon on the Financial Action Task Force’s gray list. According to a December 2023 report, the issue primarily stems from the non-financial sector, which falls outside the governor’s authority—hence, government cooperation is vital.

Monetary policy presents another significant challenge, particularly exchange rate management. The government is likely to adopt a “managed float” system requiring Central Bank intervention to defend the lira—difficult to do given the 2020 decision to halt Eurobond repayments, which severely constrained foreign currency reserves.

One of Souaïd’s most sensitive tasks will be proposing a viable banking sector restructuring plan that protects deposits while also considering accountability, which the judiciary must define. This is complicated by political divisions. Most parties fear the political backlash of deposit write-downs—technically the easiest option—yet still want to meet IMF demands, which include such write-downs.

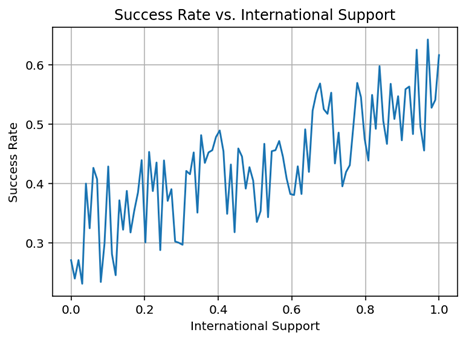

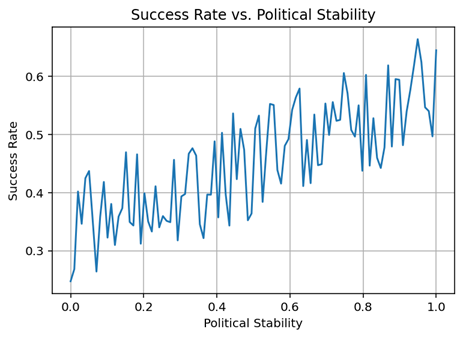

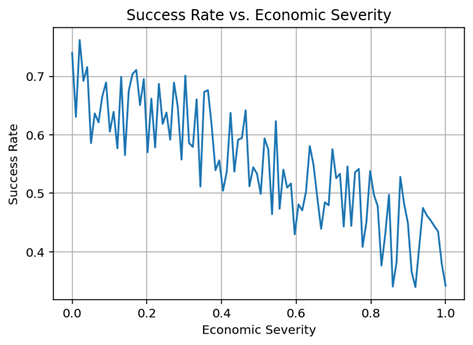

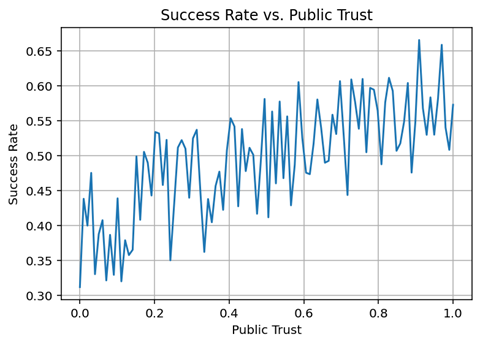

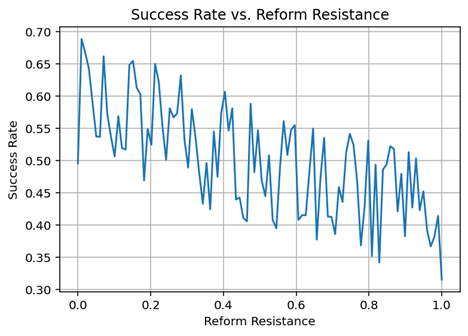

Souaïd’s success hinges on his ability to effectively manage these challenges and craft strategies that balance deposit protection, financial sector health, and currency stability. However, other factors are equally crucial: political stability, economic conditions, public trust, reforms, and international support.

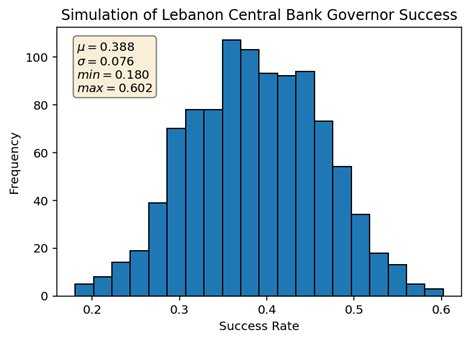

A scientific simulation we conducted to assess the likelihood of his success, factoring in these variables, estimated his chances to range between 18% and 60%, with an average probability of 40% (see Chart 2). This suggests that building external support should be a top priority if Souaïd is to boost his odds of succeeding in his mission.

Chart 2: Simulated Probability of Success for the Central Bank Governor (Source: Author’s Calculations)

Chart 2: Simulated Probability of Success for the Central Bank Governor (Source: Author’s Calculations)